Introduction:

In the realm of semiconductor manufacturing, the intricate dance between technological advancement and geopolitical tensions has never been more pronounced. As the world grapples with supply chain disruptions, burgeoning demand for chips, and the ever-looming specter of trade conflicts, the latest financial reports from the top semiconductor equipment Companies offer a nuanced glimpse into this complex landscape.

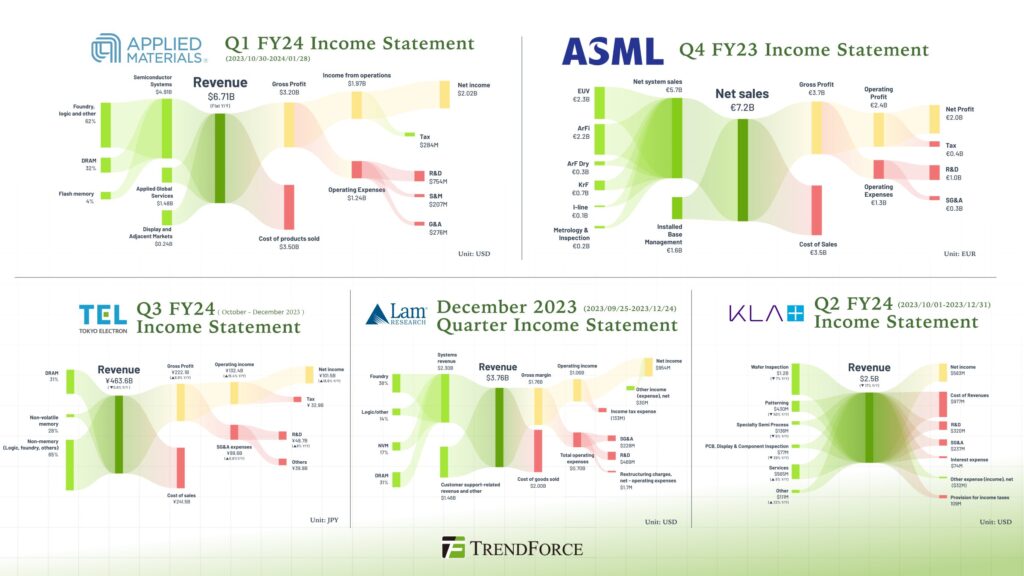

Image Credits: Trendforce

Follow us on LinkedIn for everything around Semiconductors & AI

Top 5 Semiconductor Equipment Companies Revenue

Applied Materials: Weathering the Storm

Applied Materials reported earnings of US$6.71B in 1Q24, marking a less than 1% decline in revenue. Notably, the Chinese market doubled its revenue to $3B last quarter, emerging as a bright spot for the company. This surge propelled China’s revenue share from 17% a year ago to 45%. Despite not expecting to maintain the current growth rate, Applied Materials believes the continued demand for more chips will drive market development.

While the company saw a marginal decline in revenue, its foray into the Chinese market proved promising. With a substantial jump in revenue from China, driven by the country’s ambitious plans to bolster its semiconductor capabilities across various sectors, Applied Materials remains cautiously optimistic about future growth prospects.

Read More: ASML Overtakes Applied Materials as World’s No. 1 Chip Equipment Maker in 2023 by Revenue

ASML: Navigating Choppy Waters

ASML, often regarded as a barometer for the semiconductor industry, reported 4Q23 net sales of €7.2B, up from €6.7B in Q3. With annual sales reaching €27.6B in 2023 and a 26.3% sales share in China, ASML has surpassed South Korea to become its second-largest market.

However, the company is not immune to the geopolitical tensions simmering between the US and China. Concerns over potential expansions of US export controls pose operational risks, threatening to dampen ASML’s sales to China. Despite this, ASML’s resilience and adaptability position it as a key player in navigating the turbulent geopolitical landscape.

Read More: ASML Exceeds Expectations in Q4, but Buckles Up for a Flat Sales in 2024

Tokyo Electron (TEL): Riding the Wave

TEL posted 3Q24 revenues of ¥463.6B, with China accounting for 46.9% of its revenue, a 42.8% QoQ increase. TEL expects continued strong demand from China, noting that the country produces only a small portion of the chips it needs and will actively invest to reduce reliance on foreign technology. This momentum is expected to continue into 2025.

With nearly half of its revenue emanating from China and a positive outlook for the future, TEL is poised to capitalize on the country’s concerted efforts to reduce reliance on foreign technology. As China ramps up investments in domestic semiconductor production, TEL stands to benefit from this strategic shift in the global semiconductor ecosystem.

Read More: What are Top 10 Global Data Center Markets

Lam Research: Embracing Innovation

Lam Research saw a 7.9% QoQ increase in 2Q24 revenue to $3.76B. This is with the share of revenue from the Chinese market decreasing from 48% to 40%. With the semiconductor industry expected to grow robustly in the coming years, driven by innovations like AI, Lam Research is poised to benefit. The company expects equipment expenditures by DRAM manufacturers to grow due to increased HBM production and process transitions. NAND manufacturers’ expenditures will further strengthen with technological upgrades.

With advancements in artificial intelligence fueling demand for chips and technological upgrades driving expenditure in semiconductor manufacturing, Lam Research is well-positioned to capitalize on emerging opportunities. The company’s strategic focus on DRAM and NAND manufacturers further solidifies its stance as a key player in the semiconductor equipment market.

Read More: A Day in the Life of an Etch fab Engineer

KLA: Navigating Uncertain Terrain

KLA reported a 16.7% YoY decrease in 2Q24 revenue to $2.487B. This is with China remaining its largest revenue contributor, though its share dropped from 43% in Q1 to 41%. Company estimates a mid-point revenue of $2.3B for this quarter. The demand for wafer fabrication equipment is expected to reach the higher end of the $80B range in 2024, with the second half of the year anticipated to outperform the first.

However, the fluctuating revenue share underscores the volatility and uncertainty inherent in navigating geopolitical headwinds. With projections hinting at a potentially challenging road ahead, KLA remains cautiously optimistic. The company is anticipating an uptick in demand for wafer fabrication equipment in the latter half of 2024.

Here’s a table summarizing the key financial data for each company:

| Company | Quarter/Year | Revenue | Revenue Change | Revenue Share in China |

|---|---|---|---|---|

| Applied Materials | 1Q24 | US$6.71B | Less than 1% | 45% |

| ASML | 4Q23 | €7.2B | Up from Q3 | 26.3% |

| TEL | 3Q24 | ¥463.6B | 42.8% QoQ | 46.9% |

| Lam Research | 2Q24 | $3.76B | 7.9% QoQ | 40% |

| KLA | 2Q24 | $2.487B | 16.7% YoY | 41% |

Conclusion: Charting a Course Forward

The semiconductor industry finds itself at a crossroads, grappling with geopolitical tensions that threaten to disrupt supply chains and hinder market growth. As US export controls on China continue to cast a shadow over the industry, semiconductor equipment companies must remain vigilant and adaptive in navigating this challenging terrain.